Global GDP Themes and Forecasts

The disinflation trend appears intact in the US and in the euro area. While economic growth in these regions could ease, we believe solid...

Mortgage rates have been forced higher and lending standards tighter, while oil prices have moved above $90 per barrel and the US dollar has hit new highs for the year. These factors will continue to tighten financial conditions and help move inflation back toward the Federal Reserve’s (Fed’s) goal of 2.0%.

Will these late-cycle dynamics lead to a soft landing, no landing or a hard landing? So far, US markets do not seem close to pricing in a hard landing given resilient GDP growth in 2023, elevated equity prices and tight credit spreads. However, European GDP growth has stagnated close to zero for three quarters while China’s economy remains mired in deflation as

its property bust continues. Can the US remain an island of stability in an increasingly unstable global economy?

We will explore these credit cycle dynamics to provide insights as we start to look toward 2024.

Macro DriversIn our view, the shape of fiscal policy has been an important driver of where the major countries are currently in the global credit cycle. In terms of positioning, we see the US in late cycle with heightened risks of heading into a downturn, Europe on the brink of a downturn and China in a downturn.

|

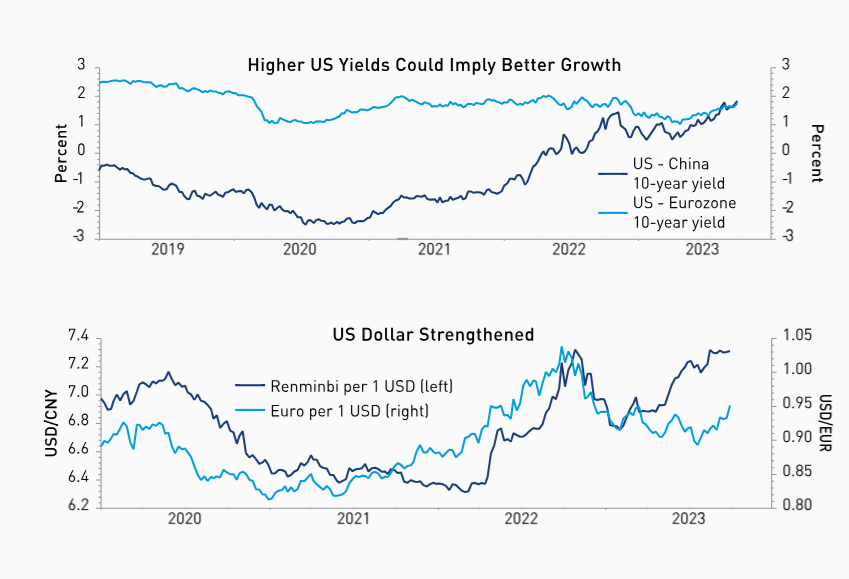

US Yields Moved Higher Year to Date Based on Economic Growth and Uncertainty Surrounding Funding the Fiscal DeficitThe focus of Chinese and European fiscal policies did not result in higher yields relative to those of the US.

Source: LSEG Datastream, data as of 27 September 2023. This material is for informational purposes only and should not be construed as investment advice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. Past market experience is no guarantee of future results. |

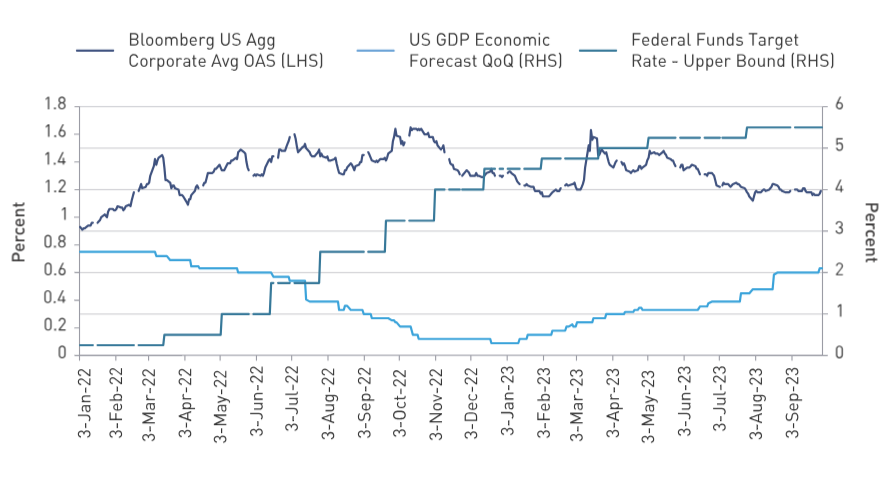

Corporate CreditDespite the fed funds rate rising to an upper bound of 5.5%, GDP growth expectations for 2023 have steadily risen to 2.1%, which in our view has been a critical factor supporting riskier corporate credits.

|

Counter to Expectations for 2023, an Economic Recession Did Not MaterializeWhen credit spreads peaked in October 2022 they coincided with a bottom in GDP growth expectations for 2023, setting up a risk-on environment.  |

Government Debt & PolicyEconomic growth expectations in the US have increased, contributing to investors anticipating a “higher for longer” fed funds rate.

|

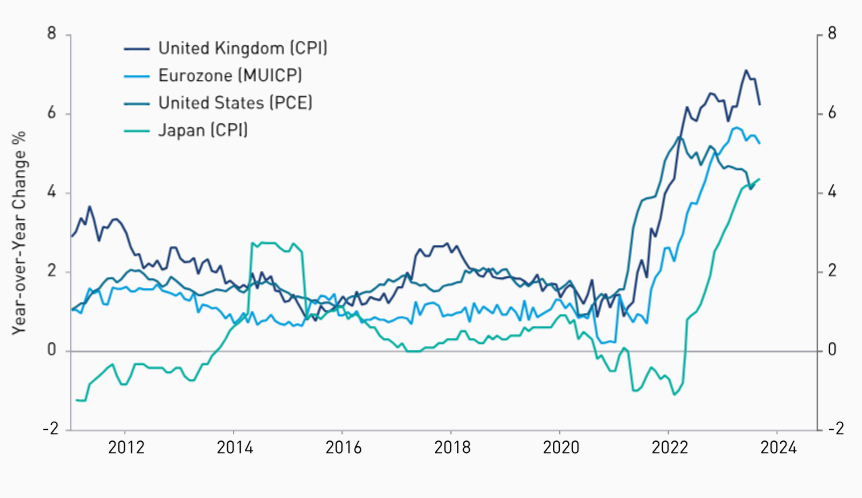

Globally, Inflation Rates Continue to Be Higher Than Central Banks’ Preferred TargetsHigher yields tend to tighten monetary conditions, which can undermine  |

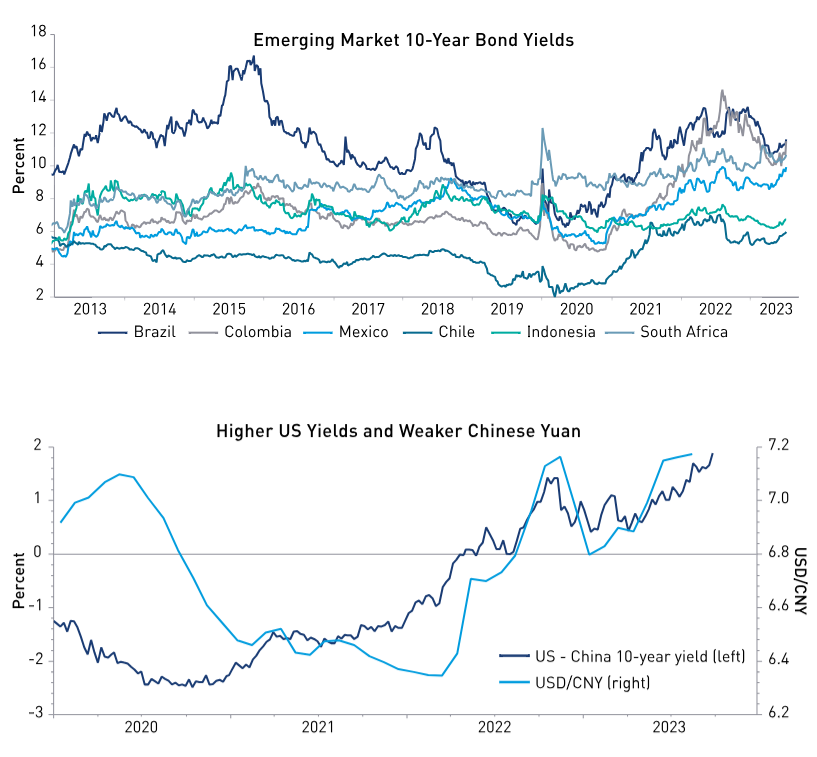

CurrenciesDownturn phases of the credit cycle are most often associated with the US dollar outperforming foreign currencies. We often remark that when bad things happen globally, the US dollar rallies.

|

Emerging Market Countries Are Currently Posting Higher Rates Relative to That of the USThe Chinese renminbi is an important anchor for many EM currencies and

Source: LSEG Datastream, data as of 27 September 2023.. This material is for informational purposes only and should not be construed as investment advice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. Past market experience is no guarantee of future results. |

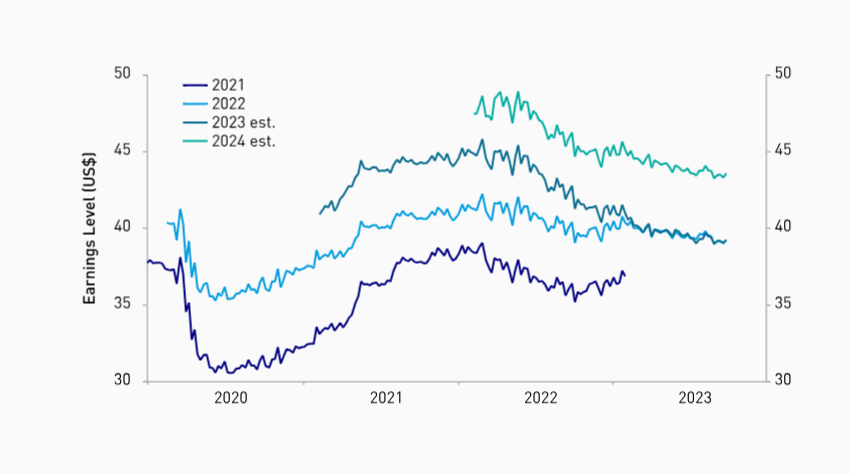

EquitiesNotably, the market seems to be expecting a robust rebound in earnings for 2024, close to 10%. We expect a much more challenging earnings environment.

|

Consensus Estimates for MSCI All Country World EarningsThe consensus global earnings rebound of plus 10% for next year is very

Sources: LSEG Datastream, IBES, data as of 27 September 2023.. Any opinions or forecasts contained herein reflect the current subjective judgments and assumptions of the Macro Strategies team only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice. This material is for informational purposes only and should not be construed as investment advice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. |

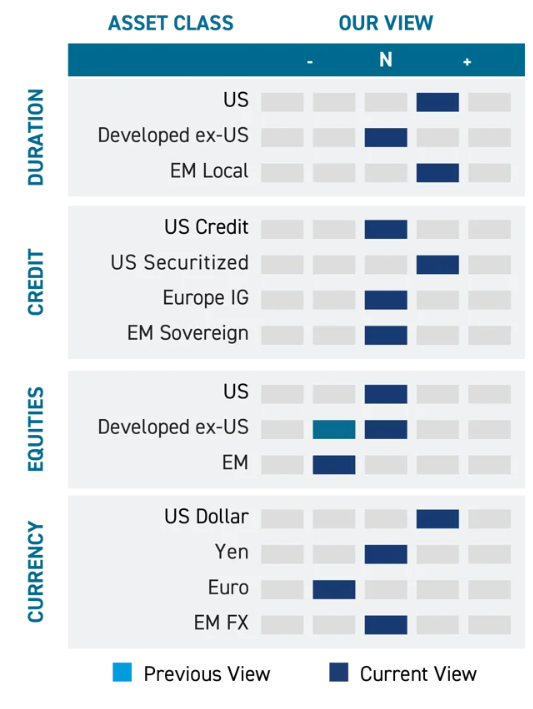

Potential RisksIn our view, a cautious asset allocation stance with a tilt toward fixed income is warranted given macroeconomic headwinds and a corporate profits recession appearing to take hold.

|

Asset Class OutlookWe are constructive on duration and neutral on credit. We would look to add growth equity exposure on weakness.

|

Senior Global Macro Strategist,

Co-Director of Macro Strategies

This article has been prepared and distributed by Natixis Investment Managers Australia Pty Limited AFSL 246830 for the Loomis Sayles Global Equity Fund (the “Fund”) and may include information provided by third parties. The information in this report is provided for general information purposes only and does not take into account the investment objectives, financial situation or needs of any person. Investors Mutual Limited AFSL 229988 is the responsible entity of the unquoted and quoted class units of the Fund. Loomis Sayles & Company, L.P. is the investment manager.

This information should not be relied upon in determining whether to invest in the Fund and is not a recommendation to buy, sell or hold any financial product, security or other instrument. In deciding whether to acquire or continue to hold an investment in the Fund, an investor should consider the Fund’s Product Disclosure Statement and Target Market Determination, available on the website www.loomissayles.com.au or by contacting us on 1300 157 862. Past performance is not a reliable indicator of future performance. There is no guarantee the performance of the Fund or any particular rate of return. It may not be reproduced, distributed or published, in whole or in part, without the prior written consent of Natixis Investment Managers Australia Pty Limited and IML.

Register to receive regular performance updates and regular insights from the Loomis Sayles investment teams, featured in the Natixis Investment Managers Expert Collective newsletter.

Loomis Sayles marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected on behalf of Loomis, Sayles & Company, and Investors Mutual Limited (the RE for Fund) by Natixis Investment Managers Australia. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.