Global GDP Themes and Forecasts

The disinflation trend appears intact in the US and in the euro area. While economic growth in these regions could ease, we believe solid...

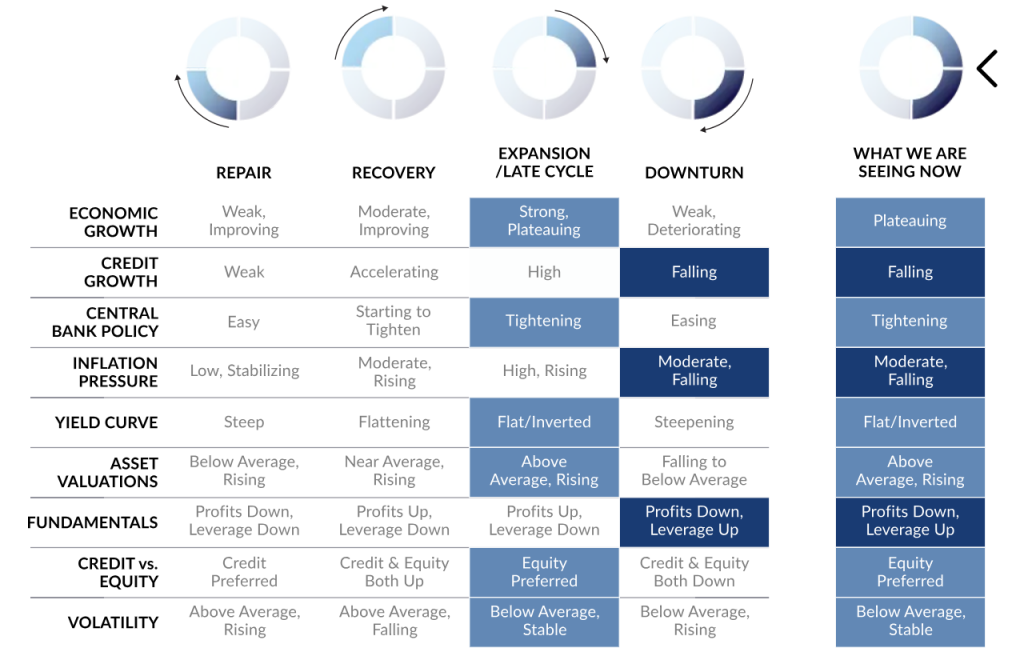

Analyzing the credit cycle involves measuring the changing factors that influence its movement and tracking the complex interactions between credit and asset prices. We use our credit cycle framework to interpret data and shape our views on where a country, sector or issuer may be in the credit cycle.

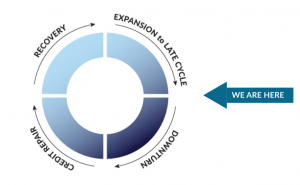

As shown in the table below, we track a few key economic indicators that, in our observation, tend to behave differently in each phase of the credit cycle. We believe the behavior of these key variables indicates the US economy continues to be in the late cycle phase of the credit cycle.

Table Source: Loomis Sayles. Views as of 21 November 2023. Highlighted cells represent attributes we’re currently observing. Lighter blue represents attributes typical of expansion/late cycle and navy blue represents attributes typical of downturn. The table presented is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and therefore, should not be the basis to purchase or sell any securities.

Forecasting Economic ScenariosUsing the credit cycle framework, we seek to join art and science and model potential future economic scenarios. We are careful to acknowledge uncertainty surrounding indicators, which can shift in large and small ways and undermine market sentiment and valuations. For example, while we believe odds of a soft landing in the next six months are high, we continue to monitor the potential impact of tighter monetary policy driving the global economy into a downturn. Looking forward, how will these variables evolve? What economic scenario will emerge? Will the late cycle dynamics we are seeing lead to a soft landing, no landing or hard landing? |

|

Graphic Source: Loomis Sayles. Views as of 21 November 2023. The graphic presented is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. Any opinions or forecasts contained herein reflect the current subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

SOFT LANDING Scenario Characteristics

|

Alternative ScenariosOne of the factors that helps the Macro team avoid “group think” is our analysts’ constant reassessments of data. Each person across the globe has an opinion based on their perspective and interpretation of the data. While at this point in the cycle the majority of the team conclude the markets can discount a soft landing into 2024 valuations, we consistently listen and learn from the analysts who foresee different scenarios unfolding. For example, some on the team believe there will be “no landing” because they expect interest rates to stay higher for longer, inflation to be stickier, and economic data to be more resilient—especially as profits in the US rebound. In such a scenario, the economy would keep growing around trend level, the labor market would remain tight and inflation would not decline as quickly as investors expect. As this scenario progressed, we could see markets come to expect the Fed to move rates higher especially versus the almost 100 basis points of rate cuts priced into the market for 2024. At current valuations, we would expect volatility in risk markets to increase as fears built of further tightening toward 6.0% on the fed funds upper bound. A much less favorable scenario could develop and the economy could go into a downturn. Deteriorating corporate profits and consumer health could tip the economy into recession. Weak demand would contribute to unemployment spikes and a decreasing risk appetite. |

NO-LANDING Scenario Characteristics

|

HARD LANDING Scenario Characteristics

|

Fiscal PolicyOur view: Fiscal policy has been an important driver of where the major countries are currently in the global credit cycle. The details: Fiscal stimulus has provided significant support for the US consumer and corporate sector since the pandemic. The funding helped shore up private sector balance sheets and left them more resilient to tighter monetary policy. |

ConsumerOur view: Excess savings is likely responsible for such a strong post-COVID recovery, but we are likely reaching the end of the line. The details: Time is ticking on the consumer’s ability to stay afloat. Student loan payments resuming do not help matters either. Slowdown in consumer spending but not going negative. |

Global GrowthOur view: The US has remained resilient so far, supported by a strong consumer. Chinese growth has disappointed while European growth is largely stagnant. The details: The US economy continues to hold in, backed by solid consumption. European growth is essentially stagnant, as major economies have seen GDP hover +/- 0% in recent quarters. Purchasing Manager Indices look weak. China’s growth story remains disappointing. Policymakers have introduced easing measures, but the property sector still faces challenges, along with the broader economy. |

Monetary PolicyOur view: Central banks are most likely done tightening. As inflation decelerates toward target levels of close to 2.0%, some may be able to cautiously cut rates. The details: Monetary policy is working with a lag. In the US, the consumer and corporate sectors have yet to feel the full impact of the tightening cycle. The Fed and other central banks may have stopped hiking, but we are a long way off from interest rates cuts. |

US Corporate ProfitsOur view: Aggregate corporate health is deteriorating but not crashing. The details: Our analysts currently see a marginal improvement in profit margins. Their overall outlook is more favorable than it was six months ago. Despite the positive trajectory, we believe caution is still warranted. We see signals that the US corporate earnings recession could be ending, but tighter financial conditions could slow economic growth and pose another challenge to balance sheet metrics. |

Credit Risk Premium/Risk AppetiteOur view: Gross Domestic Product (GDP) growth expectations for 2023 have steadily risen to 2.1%,3 which in our view has been a critical factor supporting riskier corporate credits. The details: Given the “risk-on” environment year to date, we view credit spreads as tight. While a soft landing scenario could allow spreads to remain in a tight range, there remains elevated odds that spreads leak wider over the next 6 to 12 months. |

Global InflationOur view: We are past peak inflation in major economies like the US and Europe, but questions remain regarding the speed of deceleration from here. The details: In the US, there is still a long way to go before victory against inflation can be confidently declared. We pay close attention to wages given their tight relationship with service prices. The labor market remains tight in the US, but we have seen some loosening with unemployment up to 3.9%, the participation rate ticking up further, the quit rate falling, and payroll growth cooling. |

The US DollarOur view: The dollar is expensive. The details: The relative strength of the US economy has been supportive of the dollar. A risk to a bullish outlook for the dollar would be growing expectations for the Fed to cut rates. There are many emerging market currencies that offer higher interest rates compared to the US. |

ChinaOur view: There are positive signs of recovery, but the pace of recovery remains soft. The details: China’s government appears to be more focused on deleveraging and supporting the corporate sector while consumers remain very cautious. Household consumption continued to improve through Q3 2023, particularly for services, but the gains were not strong enough to fully offset the shock to goods sectors. Property is still not out of the woods yet, housing sales weakened again in November 2023. |

GeopoliticsOur view: For the time being, we do not expect geopolitics to have a material effect on the credit cycle. The details: Countries involved in war face idiosyncratic risks; however, we do not believe wars in Ukraine and the Middle East will have a substantial effect on global growth or inflation at this juncture. We are continually assessing this view as geopolitical situations can unfold in unexpected ways. |

1 Bureau of Labor Statistics, as of 14 November 2023.

2 Quit Rate represents voluntary separations by employees (excluding retirements).

3 Source: Federal Reserve Bank of St. Louis, as of 21 November 2023.

By the Loomis Sayles Macro Strategies Team

This article has been prepared and distributed by Natixis Investment Managers Australia Pty Limited AFSL 246830 for the Loomis Sayles Global Equity Fund (the “Fund”) and may include information provided by third parties. The information in this report is provided for general information purposes only and does not take into account the investment objectives, financial situation or needs of any person. Investors Mutual Limited AFSL 229988 is the responsible entity of the unquoted and quoted class units of the Fund. Loomis Sayles & Company, L.P. is the investment manager.

This information should not be relied upon in determining whether to invest in the Fund and is not a recommendation to buy, sell or hold any financial product, security or other instrument. In deciding whether to acquire or continue to hold an investment in the Fund, an investor should consider the Fund’s Product Disclosure Statement and Target Market Determination, available on the website www.loomissayles.com.au or by contacting us on 1300 157 862. Past performance is not a reliable indicator of future performance. There is no guarantee the performance of the Fund or any particular rate of return. It may not be reproduced, distributed or published, in whole or in part, without the prior written consent of Natixis Investment Managers Australia Pty Limited and IML.

Register to receive regular performance updates and regular insights from the Loomis Sayles investment teams, featured in the Natixis Investment Managers Expert Collective newsletter.

Loomis Sayles marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected on behalf of Loomis, Sayles & Company, and Investors Mutual Limited (the RE for Fund) by Natixis Investment Managers Australia. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.